Options contracts tied to ether (ETH) worth $2.3 billion are set to expire on dominant crypto derivatives exchange Deribit this Friday.

Ahead of the pivotal quarterly settlement, the market is witnessing a low spread between Deribit’s forward-looking 30-day implied volatility index for ether (ETH DVOL) and bitcoin (BTC DVOL).

According to Deribit, the negative spread indicating relative ether stability results from an increased institutional interest in “overwriting” or selling ether call options. The dynamic has set the stage for major market shifts around Friday’s expiry.

Overwriting involves selling or writing overvalued call options or bullish derivative bets, typically against long-term buy-and-hold positions. It’s a popular way of generating additional income on top of spot market holdings. A call seller offers protection to the buyer from price rallies in return for a fixed compensation.

Since the beginning of the year, the market has seen large reflective overwriting flows in ether, which have lowered ETH implied volatility. Implied volatility (IV) refers to traders’ expectations for price turbulence and is positively impacted by the demand for options.

With June contracts set to settle this Friday, overwriters may roll over their positions. In other words, short positions expiring on Friday may be squared off and moved to the July or September expiry. That could cause significant shifts in how IV is priced in the bitcoin and ether markets.

“ETH has witnessed substantial institutional selling activity [in call options], earning a trader the moniker of the ‘ETH overwriter’ aka an ETH volatility selling whale! Remarkably, this has resulted in a scenario where DVOL (implied volatility index similar to VIX) in ETH is lower than that of BTC,” Deribit’s Chief Risk Officer Shaun Fernando told CoinDesk.

“As these substantial positions near their expiration, it could lead to captivating shifts in volatility as participants consider rolling over their positions,” Fernando added.

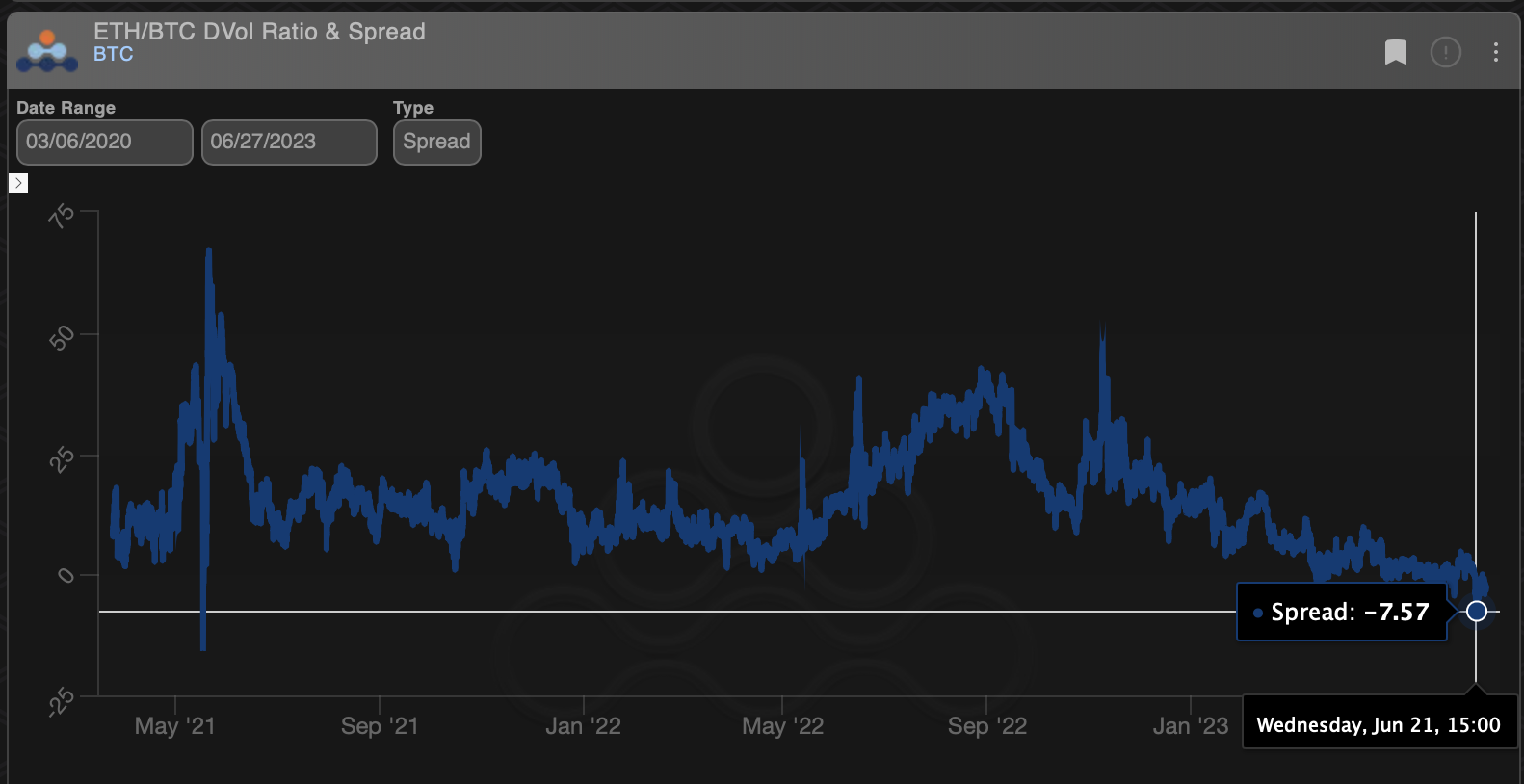

The spread hit a three-year low last week (Amberdata)

At press time, the ETH-BTC DVOL spread stood at -2.5, having hit a three-year low of -7.8 last week, according to data source Amberdata. Implied volatility, or IV, represents traders’ expectations for price turbulence over a specific period and is positively impacted by the demand for options. A call option represents a bullish bet on the underlying asset, while a put represents a bearish bet.

While rollovers may influence the ETH-BTC DVOL spread, ether’s price is likely to stay around $1,800-$1,900, according to over-the-counter liquidity network Paradigm.

“In terms of ETH dealer gamma heading into expiry, we predict $1,800-$1,900 strikes to be a magnet for spot, predominantly because dealers have largely got long due to previously discussed overwriter flows,” Paradigm said in its market update.

Being long gamma means holding buy (long) positions in options. When market makers are long gamma, they buy low and sell high to keep their overall exposure market neutral. The hedging often ends up keeping prices rangebound.

I have the unfortunate duty of informing you that this is the last edition of The Airdrop. We are enormously grateful to Rosie Perper for leading this project and to various other members of the CoinDesk team who helped pull it together each week. Sadly, after a round of layoffs and cost-cutting at CoinDesk this…

news In a dramatic bit of stagecraft, BitMEX has finally released the “tapes” from its so called Tangle In Taipei, a July 3 debate between CEO Arthur Hayes and NYU Professor and so-called Dr. Doom, Nouriel Roubini. It even comes with dramatic fight music. The debate was about security and scalability where Hayes calls for…

NEWS Sep 21, 2018 at 20:30 UTC The parent company of Brazil's largest independent broker is setting up a cryptocurrency exchange, Bloomberg reported Thursday. Grupo XP, which owns brokerage firm XP Investimentos, plans to launch the platform in the "coming months," the news source said, adding it will support trading in bitcoin and ethereum. However,…

markets View Bitcoin created a doji candle yesterday, signaling buyer exhaustion near the crucial 21-week moving average (MA) resistance at $4,073. As a result, a price pullback could be in the offing in the next 24 hours. A break below $3,930 (flag support on 4-hour chart) would further strengthen the case for a pullback and…

Posts on X from Coinbase and Base creator Jesse Pollack suggest the crypto exchange is developing a wrapped bitcoin similar to Bitgo's wBTC to run on the layer-2 blockchain. Despite some controversy over wBTC, BitGo's protocol remains stable. 02:29 Crypto Goes Unmentioned in Trump-Musk Interview; 3AC Liquidators Suing Terraform Labs for $1.3B 01:04 Bitcoin Above

Jun 30, 2020 at 21:30 UTCSpanish police arrested 33 suspects during their parallel drug raids. (Wikimedia commons)Spain’s National Police on Sunday arrested 33 people who allegedly sold illegal medications online and laundered at least part of their €3 million ($3.37 million) profit in virtual currency. The busts, conducted against two separate organizations, resulted in the…

The security tokens issued by Sygnum Bank represent Matter Labs' investment in a Fidelity International money-market fund.Tokenization of traditional assets is a growing phenomenon at the intersection of crypto and traditional finance that has attracted several banking giants to develop offerings.00:34Market Maker KeyRock Secures Swiss Anti-Money Laundering Clearance02:21Sam Bankman-Fried's Lawyers Push for FTX Founder's Jail

news The U.S. Securities and Exchange Commission (SEC) may make an initial decision on not one, but two different bitcoin exchange-traded fund (ETFs) proposals by April 5. A bitcoin ETF proposal submitted (for a second time) by VanEck, SolidX and the Cboe BZX Exchange is expected to be formally published in the Federal Register Wednesday, kicking…