For the past nine months, overall macro conditions have taken a back seat to the idiosyncratic failures (FTX, Terra’s LUNA/UST, BlockFi, CoinDesk sister company Genesis) and success stories (the Ethereum Merge, various layer 2 launches) that drove most of the price action. But macro regained its position behind the wheel over the past few weeks. The banking crisis and subsequent policy response have taken center stage – only this time it is affecting digital assets positively at the expense of other asset classes. A quick look at the bitcoin (BTC) price versus the regional banking exchange-traded fund (KRE) tells you all you need to know about the winners and losers since the first week of March.

Jeff Dorman, CFA, is chief Investment officer and co-founder of Arca.

(Bloomberg)

While digital assets gain, macro investors are dipping back into the recession playbook:

Front-end rates are down sharply, while long rates are only slightly lower (bull steepener – a classic recession trade).

Gold is ripping and closing in on an all-time high.

Crude oil is getting smoked.

Small caps and growth stocks are underperforming large caps and value stocks, while defensives are leading cyclicals.

Technology is getting valuation support from falling rates.

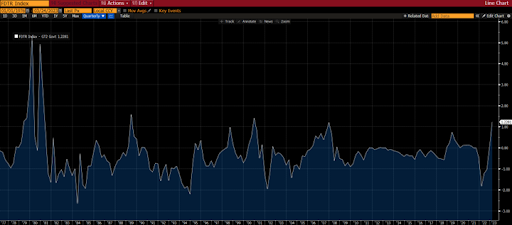

The U.S. Federal Reserve has lost credibility. The two-year Treasury yield has fallen from an intra-month high of 5.08% to its current 3.75% yield, which is a startling enough move as it is. It is even more dramatic when you factor in the Federal Reserve’s decision to raise its benchmark rate 25 basis points (bps) to 5% at the same time.

That’s the market’s way of telling you it’s calling the Fed’s bluff. The fed funds rate started the month below the two-year yields, and is currently 125 bps higher. This spread is now the largest between the fed funds rate and two-year Treasury yield since 2007 and has historically led to quick and aggressive rate cuts.

Spread between fed funds rate (upper bound) and two-year Treasury Yield. (Bloomberg)

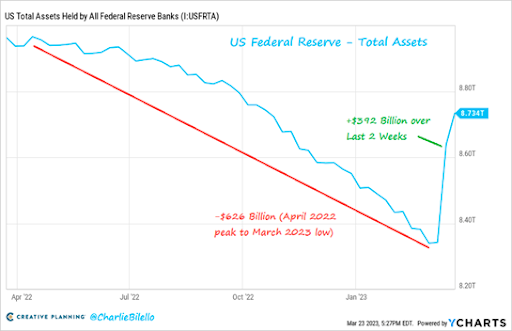

Further, the “Fed put” is back in play as assets on the central bank’s balance sheet increased by $392 billion over the last two weeks, wiping out 60% of the value of the quantitative tightening done since last April.

(via Twitter @charliebilello)

Not to be outdone, the Treasury Department has also lost credibility. After joining the Fed and the Federal Deposit Insurance Corporation in their explicit defense of depositors of a select few failed regional banks, Treasury Secretary Janet Yellen can’t decide whether to offer full support explicitly or instead avoid moral hazard. In the last three days Yellen has flip-flopped multiple times on her position regarding an increase in the level of deposit insurance. Yellen’s previous remarks on the state of the economy haven’t aged well. In 2017, she confidently stated that she didn’t believe we would see another financial crisis “in our lifetime.”

And lest we forget about Credit Suisse – a forced shotgun marriage to UBS left shareholders and many CoCo bondholders dead or nearly dead, but the Swiss bank has been a problem child for at least 15 years. As Bloomberg reported:

“Credit Suisse’s failings have included a criminal conviction for allowing drug dealers to launder money in Bulgaria, entanglement in a Mozambique corruption case, a spying scandal involving a former employee and an executive and a massive leak of client data to the media. Its association with disgraced financier Lex Greensill and failed New York-based investment firm Archegos Capital Management compounded the sense of an institution that didn’t have a firm grip on its affairs. Many fed-up clients have voted with their feet, leading to unprecedented client outflows in late 2022.”

Ironically, trying to kill crypto while saving the banks ultimately saves crypto, too.

With this backdrop – a Fed that has lost control, a Treasury secretary who has lost touch and an accelerating global banking crisis – it’s perhaps not surprising that crypto app downloads jumped 15% last week while those of banking apps have fallen around 5%. The market is showing its lack of confidence in our governments and financial systems via a renewed interest in a potential alternative – which is hilarious when you consider that this increase in crypto adoption is happening concurrently with the Security and Exchange Commission’s war on digital assets.

The SEC most recently issued an investor alert urging caution when investing in digital assets, which reads fine and accurate in isolation – you should be cautious when investing in digital assets. But the timing of this statement, amid a series of other enforcement actions for the year to date, seems disingenuous considering all of the other much larger problems in the global financial markets. Meanwhile, the SEC also sent Coinbase a Wells Notice, setting the stage for an epic court battle between two obstinate behemoths.

Try as the SEC, Treasury, White House and Fed may, there’s just no way to put the genie back in the bottle at this point. The bull case for crypto is on full display as banks shutter and their depositors and investors hit the eject button. Granted, this will cause operations and the flow of capital to be even more cumbersome for digital asset participants as well. We are already starting to see the effects as liquidity is sucked out of the digital assets spot market.

However, the real battle isn’t between digital asset investors and regulators but between banks and stablecoin issuers. Stablecoin issuers still depend on banks to keep their reserves, and banks have been very resistant to help a sector that is trying to put them out of business – which, of course, makes sense.

Arthur Hayes wrote a great piece at the end of 2022 about the friction between banks and stablecoins before any of the banking failures commenced. The very heart of the problem is that rising rates is great for stablecoin issuers because they keep all of the interest income themselves and pass none of it on to token holders, whereas rising rates cause a real problem for banks who lose depositors when they don’t pass along the interest, and also become underwater on their longer-term loans. Here is what he said:

“… [D]o you understand why banks HATE these monstrosities? Stablecoins do banking better than banks since they operate on almost 100% profit margins. Any time you read FUD about this or that stablecoin, just remember: the banks are just jealous.”

And getting rid of current iterations of stablecoins in favor of a central bank digital currency (CBDC) isn’t much better. In a 2022 report, McKinsey estimated that globally banks stand to lose $2.1 trillion in annual revenue if a successful retail CBDC is introduced.

The reality is, even though we are trying to build a digital infrastructure that runs in parallel to the existing financial system, the ecosystem is still very intertwined with the traditional banking system. So, ironically, trying to kill crypto while saving the banks ultimately saves crypto, too. It’s a win-win right now for blockchain enthusiasts.

Disclaimer: This commentary is provided as general information only and is in no way intended as investment advice, investment research, legal advice, tax advice, a research report, or a recommendation.

Edited by Ben Schiller.

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

DISCLOSURE

Please note that our

privacy policy,

terms of use,

cookies,

and

do not sell my personal information

has been updated

.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a

strict set of editorial policies.

CoinDesk is an independent operating subsidiary of

Digital Currency Group,

which invests in

cryptocurrencies

and blockchain

startups.

As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of

stock appreciation rights,

which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG

A Bitcoin Core dev and her exchange partner discuss Bitcoin and privacy and how to incentivize more developers to contribute to the protocol. For more episodes and free early access before our regular 3 p.m. Eastern time releases, subscribe with Apple Podcasts, Spotify, Pocketcasts, Google Podcasts, Castbox, Stitcher, RadioPublica, iHeartRadio or RSS. This episode is sponsored by Bitstamp and Crypto.com. OKCoin and BitMEX…

Metal Pay's "First Blockchain Bank and Trust" would be FDIC-insured, CEO Marshall Hayner told CoinDesk.The Office of the Comptroller of the Currency announced banks could provide crypto custody services in December 2020. (Matthew G. Bisanz/Wikimedia Commons)Feb 4, 2021 at 6:02 p.m. UTCUpdated Feb 4, 2021 at 6:28 p.m. UTCCrypto Startup Metal Pay Files for National…

Coinbase (COIN) shares rose over 24% Thursday after the U.S. District Court dismissed part of the Securities and Exchange Commission’s (SEC) case against Ripple Labs and ruled that the company’s XRP token is not a security, however, the extent of the rally may not be warranted, investment bank Berenberg said in a research report.“The surge…

feature Consider yourself $14.1 million closer to buying your morning coffee with bitcoin. New York-based payments startup Flexa just raised that amount in a private token sale involving Pantera Capital, 1kx, Nima Capital, Access Ventures and others. The startup’s token, Flexacoin, is an ethereum-based ERC-20 token that will eventually be used by developers and businesses…

Music megastar Taylor Swift approved a sponsorship deal with the now bankrupt crypto exchange FTX last year, despite previous reports that she had walked away after conducting her own due diligence on the firm, the New York Times reported on Thursday.In the spring of 2022, the pop star discussed a deal with FTX worth as…

A supposed cheat for the massively popular video game Fortnite turns out to be malware designed to steal bitcoin wallet login details. That's according to Malwarebytes Labs, which reported finding the malicious program on Oct. 2. An investigation by the Califonia-based cybersecurity firm followed a trail from one of many dubious videos posted on YouTube…

Decentralized finance (DeFi) lender bZx suffered a hack of reportedly $55 million, according to a tweet on Friday by the blockchain security firm SlowMist.“#bZx private key compromised, over $55 million dollars stolen so far. We’ll continue to update as more information is discovered,” SlowMist tweeted.bZx responded in a tweet that a private key controlling the…

When Gary Gensler’s Securities and Exchange Commission (SEC) this week filed securities charges against America’s biggest cryptocurrency exchange, they were premised on a single core idea: that U.S. law already includes the necessary tools to regulate cryptocurrency assets and marketplaces. Gensler, an appointee of the Biden administration, has consistently repeated that crypto doesn’t need new…

Memecoins embody the “Wild West” image of DeFi. Thanks to the stratospheric success of tokens like Dogecoin (DOGE) and Shiba Inu (SHIB), the memecoin market collectively boasts a market cap of $54.4 billion – a number that would’ve seemed outrageous when these assets first emerged. And yet here we are.As recently as March, memecoin trade

:format(jpg)/downloads.coindesk.com/arc/failsafe/user/1x1.png)