First-Quarter Performance Recap: CoinDesk Market Index Up 58%, BTC Gains Amid Banking Crisis

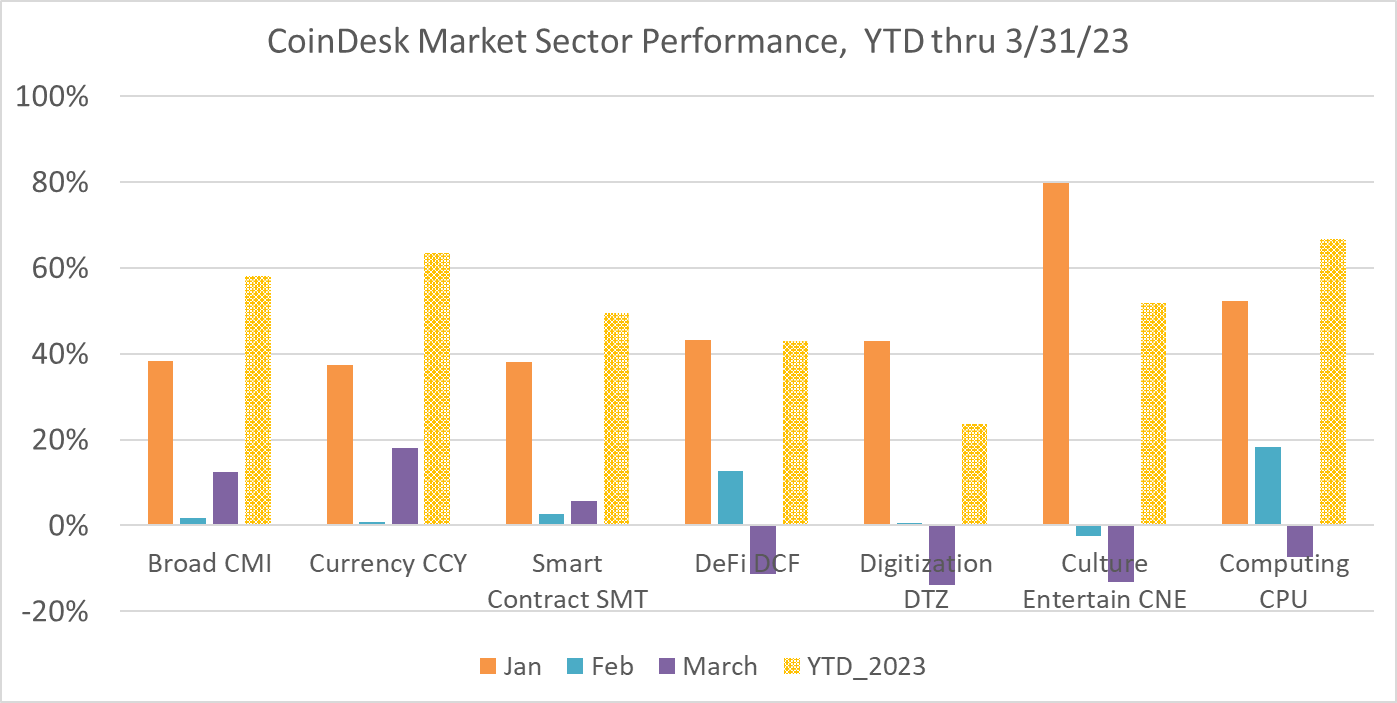

It’s been quite a start to the year in the world of crypto. Bitcoin (BTC) posted its best quarterly performance in over two years, gaining 68%, for the first three months of 2023. The broader CoinDesk Market Index, or CMI – which spans over 90% of the crypto market capitalization – is up 58% on the quarter with ether (ETH) and cardano (ADA) up 50% and 57% over the same period.

Todd Groth is head of research at CoinDesk Indices, a provider of digital asset indices since 2014.

The computing sector, or CPU (+67%), benefited from the positive sentiment surrounding artificial intelligence sparked by the the debut of ChatGPT last November. The currency sector, or CCY (+63%), benefited from the U.S. regional bank jitters and from the expansion across central bank balance sheets. January’s rebound in investor sentiment (see “January Effect”) has provided buoyancy for the broad market after a challenging 2022. Digitization, or BTZ (+24%), and DeFi, or DCF (+43%), are also positive for the year.

Figure 1: CMI Sector 2023 Performance Attribution; Source: CDI Research

So where do we go from here?

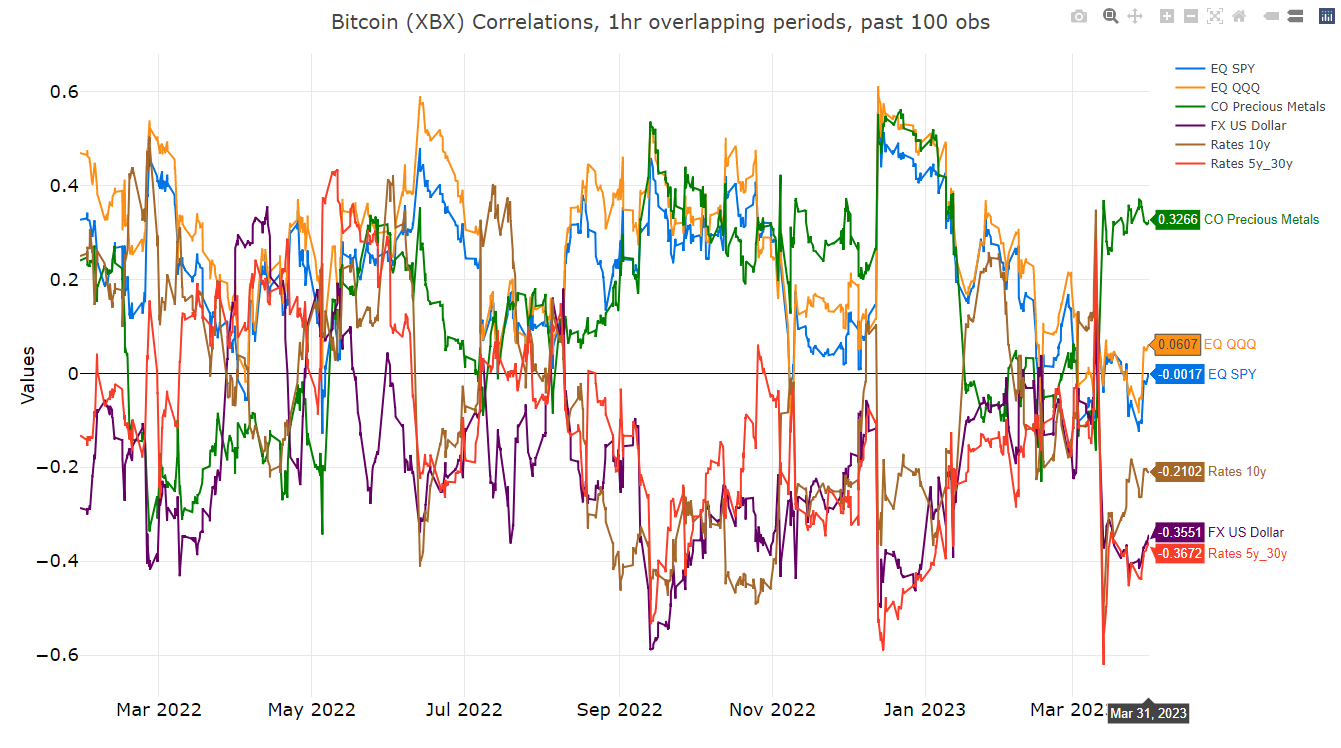

Digital assets tend to do best when they trade according to their own narrative (say like bitcoin’s inflation hedge thesis) and decouple from the factors and themes driving traditional asset classes.

So far in 2023, crypto appears to be bucking trends driving stocks and bonds, including 2022 inflation fears and quantitative-tightening at the Federal Reserve. Digital assets have less in common now with growth-oriented equities, with a lowering of correlation between digital assets and equities. Within bitcoin specifically, we’re also seeing a strengthening in the correlation with gold (positive) and the U.S. dollar (negative). The “digital gold” and fiat “currency debasement hedge” narratives re-emerge and regain investor consideration.

Figure 2: One-hour correlations between bitcoin (XBX) vs macro indexes. Source: CDI Research

Bitcoin’s 25% gain during the regional banking crisis can be attributed partly to the steepening of the yield curve in the bond market.

We continue to see a moderately negative relationship between bitcoin price changes and the yield curve slope (using the five-year to the 30-year yield spread as proxies), which is a market-derived proxy for interest-rate expectations based on U.S. Treasury bond pricing. The recent peak in U.S. yield curve inversion of +46 basis points on March 8, just before the collapse of Silicon Valley Bank, tumbled to -15 basis points as of March 27 as the market priced in fewer rate hikes and cuts post-SVB.

This 60 basis-point drop in yield curve slope (with five-year rates dropping more than 30-year rates, bull steeping), combined with the negative correlation of -0.4 between the yield curve slope and bitcoin, suggests one-third of bitcoin’s 25% gain during the regional banking crisis can be attributed to the steepening of the yield curve.

This relationship between bitcoin and the yield curve strengthened during the Silicon Valley Bank event, supporting the digital gold narrative.

With the Federal Reserve’s balance sheet continuing to expand, in a mere two weeks the new lending facilities created to mitigate the regional banking crisis in March have undone months of balance sheet tightening. The Fed’s actions come alongside continued monetary stimulus coming from the Bank of Japan (buying domestic bonds to maintain yield curve control) and the People’s Bank of China, which is stimulating an economy weakened by COVID lockdowns.

From the perspective of a digitally scarce asset like bitcoin, these are all encouraging developments. But it’s unlikely we are heading for a halcyon redux of 2021’s crypto bull market

The U.S. regional banking concerns and the rapid unwind of Credit Suisse (CS) have highlighted weaknesses in the traditional financial system when interest rates rise. While this may come to the delight or amusement of crypto maximalists and critics of the fractionalized banking system, it is a source for further deleveraging contagion risk. Most digital-asset investments share a broader portfolio with traditional public and private-asset markets, with capital allocation decisions within these portfolios linking these disparate markets together through relative value choices which promote and drive correlations across markets. Crypto cannot sail alone.

That the Fed will make fewer hikes, and more rate cuts, is pretty much priced into the market now and reflected in the yield curve steepening mentioned above. That has benefited bitcoin and gold, and at the expense of the U.S. dollar.

A portion of these rate expectations might be due to the move of investors out of banking deposits and into front-end Treasurys for corporate treasury risk-management purposes. Why hold deposits at a regional bank, when you can earn similar interest in short-term paper without the credit risk of a potentially shaky bank?

That said, the market appears to view the collapse of SVB as a pivot in the interest-rate hiking cycle. If the tightening of credit conditions and lending standards begin to percolate through the economy and inflation cools down further, then the Federal Reserve will no longer have to hike rates as the credit markets have effectively tightened financial conditions on the Fed’s behalf.

But if inflation remains persistent and elevated, the Fed will have to go against market pricing and continue to hike, which has the potential of triggering a redux of 2013’s “Taper Tantrum” and the liquidation risk mentioned above.

Liquidity in crypto markets has dropped with trading volumes post-FTX. Until prices rise enough to reignite interest from traders who exited the market in 2022, we don’t expect it to improve. With U.S. regulatory action against exchanges and the closure of a number of banks providing crypto on-ramping services, additional hurdles remain for capital entering into the digital-asset market these days.

Learn more about Consensus 2023, CoinDesk’s longest-running and most influential event that brings together all sides of crypto, blockchain and Web3. Head to consensus.coindesk.com to register and buy your pass now.

DISCLOSURE

Please note that our

privacy policy,

terms of use,

cookies,

and

do not sell my personal information

has been updated

.

The leader in news and information on cryptocurrency, digital assets and the future of money, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a

strict set of editorial policies.

CoinDesk is an independent operating subsidiary of

Digital Currency Group,

which invests in

cryptocurrencies

and blockchain

startups.

As part of their compensation, certain CoinDesk employees, including editorial employees, may receive exposure to DCG equity in the form of

stock appreciation rights,

which vest over a multi-year period. CoinDesk journalists are not allowed to purchase stock outright in DCG

.

Todd Groth is Head of Index Research at CoinDesk Indices. . He has over 10 years of experience involving systematic multi-asset risk premia and alternative investment strategies.