Bitcoin’s ‘Store-of-Value’ Narrative Is Real but Not a Price Mover

Markets are noisy, chaotic things that we human beings instinctively try to imbue with order and reason. This generally involves searching for explanations as to why prices are trending up or down or what triggered a sharp move.

Often there is an obvious explanation – an earnings surprise or an unexpected corporate action. Sometimes the cause isn’t so easy to see – flows of funds, an evolving user base, steady product development and so on.

Noelle Acheson is the former head of research at CoinDesk and Genesis Trading. This article is excerpted from her Crypto Is Macro Now newsletter, which focuses on the overlap between the shifting crypto and macro landscapes. These opinions are hers, and nothing she writes should be taken as investment advice.

With bitcoin (BTC), it’s even harder to discern what is driving sentiment shifts at any given time because it doesn’t have earnings, there are no corporate actions, regulation isn’t the threat it is for some other crypto assets and the narratives are multiple and varied. There isn’t even universal agreement as to what bitcoin is, let alone what drives its price.

But our search for reason amid chaos encourages us to latch on to something that makes sense, and if it is a narrative that justifies our interest while highlighting a timely concept, then so much the better.

One phrase we’re hearing a lot of these days is “store of value.” It tends to mean different things to different people, but in general, it refers to an asset that holds its value relative to a broad basket of other assets over a long stretch of time.

In spite of its short-term price volatility and sharp bear markets, bitcoin is a store of value because it is the only asset traded on liquid exchanges today with a programmatic and verifiable hard cap. With other “hard assets” (those with limited supply) such as gold, diamonds or real estate, we don’t know the supply cap, nor do we know how much is currently in existence.

Plus, with other “hard assets,” the price influences the potential supply. For instance, if gold were to surge from $2,000 to $20,000 per ounce, new extraction methods would become viable, boosting the theoretical cap. Bitcoin is the only asset traded on liquid exchanges for which the price has no influence whatsoever on the supply. It is the hardest of hard assets.

What’s more, the supply of its most common denominator – the U.S. dollar – has been increasing over the decades, and more recently at an astonishing pace. We are likely about to embark on another wave of monetary easing, involving lower interest rates and the incentivization of credit to overcome declining economic growth and consumption.

An increase in the supply of USD above what economic growth can absorb will – all other things being equal – decrease its value relative to other assets, and following basic math, if the value of the denominator drops, that of the ratio increases. Bitcoin is a store of value and a hedge against currency debasement.

Finally, bitcoin the asset lives on a decentralized network (confusingly also called Bitcoin, distinguished here with uppercase), which lends this store of value an almost unique degree of seizure resistance. It can be argued that other hard assets can be held “off the grid” (gold can be kept under the kitchen floorboards, and maybe no one knows about the cabin in the woods), but they are complicated to transport and can be seized. Bitcoin ownership doesn’t reside on centralized ledgers unless it is at the holder’s request, an option many choose for convenience. Even so, the asset’s inherent seizure resistance and mobility further enhance its store-of-value qualities.

![]()

![]()

Trader-led expectation of growing interest in the store of value narrative is probably behind more of the recent price move than is actual interest

![]()

![]()

Given the ballooning economic uncertainty, it makes sense that investors are looking to strengthen their portfolios with stores of value, and it makes sense that many are starting to pay more attention to this novel asset. This growing interest, we’re told, is one of the main factors behind bitcoin’s more than 80% price increase since the beginning of the year.

Only, technically, it’s not.

Stores of value are generally of interest to longer-term investors. Bitcoin’s price is set by short-term traders.

That’s not to say that the store-of-value narrative hasn’t been a key driver of bitcoin investment since the early days. In bull markets and bear, those with a long-term thesis have been steady accumulators – metrics that track the movement of bitcoin on-chain show that almost 30% of bitcoin in circulation hasn’t moved in over five years, and even during the painful drawdown of last year, that percentage continued going up and to the right (true, some of these bitcoin could be permanently lost, but the bulk of it most likely corresponds to store-of-value investors). Almost 40% hasn’t moved in over three years, over 50% hasn’t moved in over two. You get the picture.

But this steady accumulation has been quiet and consistent, and hasn’t accounted for bitcoin’s wild price swings. Those are driven by speculation on this and other narratives.

In any public market, the latest trade is what determines the price. In liquid markets, there are trades every nanosecond, and they are usually at prices close to the last one but changing preferences will move this up or down. These are usually from traders and market makers hoping to profit from short-term moves, which are influenced by narratives and news.

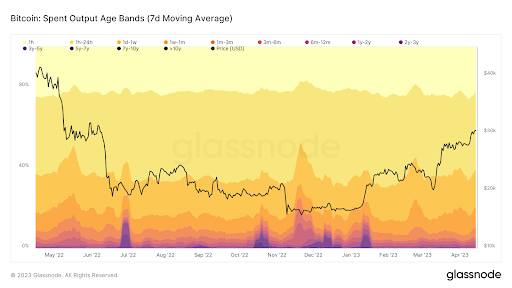

For bitcoin, while we don’t have access to the churn in exchange volumes since these happen off-chain, we do know the average age of on-chain movements. Much more trading is done off-chain than on-chain, and so we can assume that they are at least representative of the makeup of exchange volumes. The chart below from Glassnode shows that, on any given day, at least half of bitcoin transferred between addresses had last been moved within the previous 24 hours (the light and dark yellow bands). Even on-chain, the bitcoin market is high turnover, and short-term traders dominate.

So, in the case of bitcoin, the trader-led expectation of growing interest in the store-of-value narrative is probably behind more of the recent price move than is actual interest. Investors may increasingly see bitcoin as a store of value, and growing demand in the face of a fixed supply will obviously push the price up. But the bulk of price moves are from traders betting on this demand rather than actually forming part of it.

This highlights the key role narratives play in crypto markets, more so than in other markets with a steadier flow of fundamental data.

It also exaggerates price movements on the way up, and on the way down. Unlike fundamental value drivers, narratives are inflated and deflated by sentiment, which is influenced by an incomprehensible range of factors. It even ends up influencing itself.

What generally happens in bitcoin cycles is that the prevailing narrative starts out being about one thing (e.g., store of value) and ends up being about another (price). Whatever you may believe is the main story line driving current interest – store of value happens to be the one I’m hearing most about these days, but there’s also monetary liquidity, the need for banking “insurance” and more – our attention invariably pivots to price movements, which themselves end up becoming the story.

We need to keep an eye out for this because we’ve all seen how that type of narrative can push the price up (which is good) but rapidly remove support when winds change. When “price” becomes the story, we need to be aware that sentiment is becoming flimsier, because traders are no longer betting on what longer-term investors will do, they are betting on what other traders will do.

The underlying potential growth may not have changed and accumulation by those with an eye on the bigger picture will continue regardless. But sentiment and price tend to be driven by short-term market participants who are influenced by much more than a good story. This matters for market momentum, and serves as a warning against becoming too wedded to any particular narrative when it comes to trying to make sense of market moves.

Edited by Ben Schiller.