Bitcoin Prices Are Hot, but Here’s What Could Crush the Rally

We’re starting today’s column where we left the last, asking: Will macroeconomic narratives subside? The answer may ultimately be a bit nuanced. Macro factors will always play a role, but some key issues have been occurring in a relatively predictable fashion, especially as they relate to inflation.

Save for a few hiccups, inflation projections and the Federal Open Market Committee’s (FOMC) expected response with interest rates have played out as expected.

Bitcoin (BTC) prices are up 87% year to date and seem to have found support near $30,000. Ether (ETH) has risen 64%, trailing BTC but still impressive nonetheless.

You’re reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

Both have largely shrugged off this perilous period for the overall crypto industry. Something called the Anchored Volume Weighted Average Price (AVWAP) of BTC helps show that.

Volume Weighted Average Price (VWAP) is a technical indicator that lets traders determine the average price of an asset, taking volume and price into account. AVWAP does the same thing but lets traders anchor their starting point to a customized date.

Bitcoin’s AVWAP since the U.S. Securities and Exchange Commission’s lawsuits against Binance and Coinbase is 9.1% lower than where BTC currently trades. The AVWAP taken from Nov. 9, 2022, the day Binance scrapped its proposed FTX takeover, is $22,632. Anchoring from when Celsius paused withdrawals in June 2022 shows an AVWAP of $21,400.

In other words, bitcoin has bounced back from a series of bad events.

The question now is, what could go wrong? What macroeconomic developments could send prices lower, eroding the aforementioned gains?

Reading through some of the more recent speeches by Federal Reserve Chairman Jerome Powell indicates that the FOMC is resigned to continuing its current course of action.

The market appears to be expecting at least two more rate hikes in 2023, topping out around 5.6%. If that occurs, it’s difficult to imagine a significant shock to prices in either direction; it’s likely already priced in.

But there are a few other macro factors that warrant attention in crypto markets:

Banks passed the most recent stress tests

One of the largest news stories of the year was the collapse of Silvergate Bank and Silicon Valley Bank. Since both had ties to crypto, the news reverberated throughout the sector. Their failure led to thoughts that FOMC rate hikes had gone too far, creating too much stress among banks.

However, recent stress tests that were administered to 23 systemically important banks showed they appear to be well-positioned to weather a severe recession and continue lending to qualified households. The test assumed an unemployment rate of 10%, a 40% decline in commercial real estate and a 38% decline in housing prices.

The FOMC may feel that it has enough room to aggressively raise rates, despite the impact that may be felt. Subsequent weakness in the economy would be painful but would likely bring inflation down without cratering the banking system.

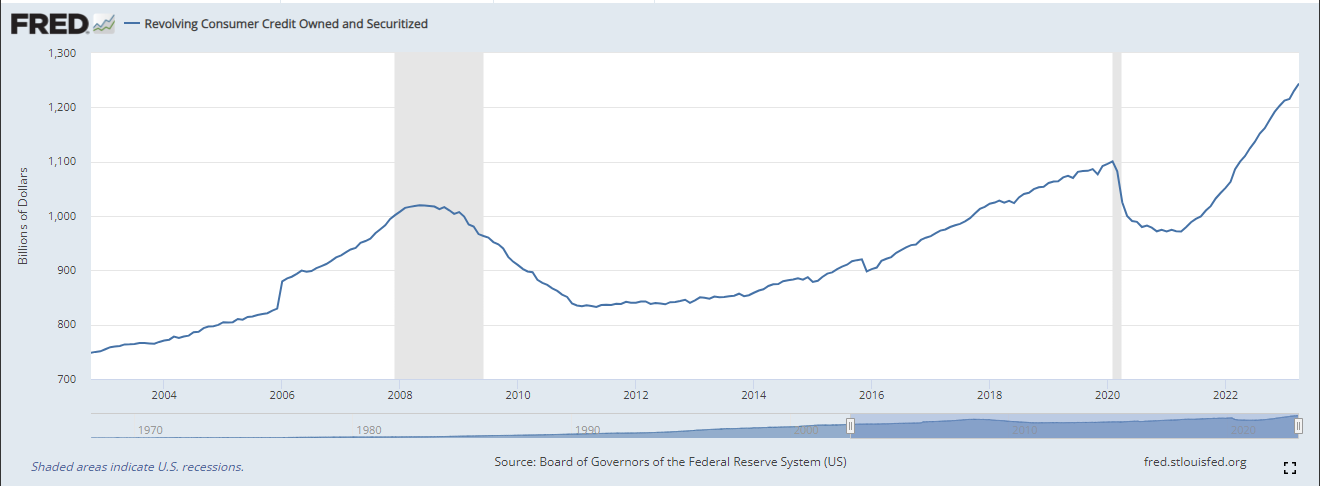

Consumer revolving debt continues to rise

Revolving debt is at all-time highs. This is an area that doesn’t get a ton of attention, but is still significant.

Crypto investing continues to have a large retail component. Glassnode data show 1.3 million BTC held by investors with less than 1 bitcoin, and that population has grown 73% since 2021.

Increases in credit balances in conjunction with higher interest rates and potentially lower employment concern me as far as crypto investing is concerned.

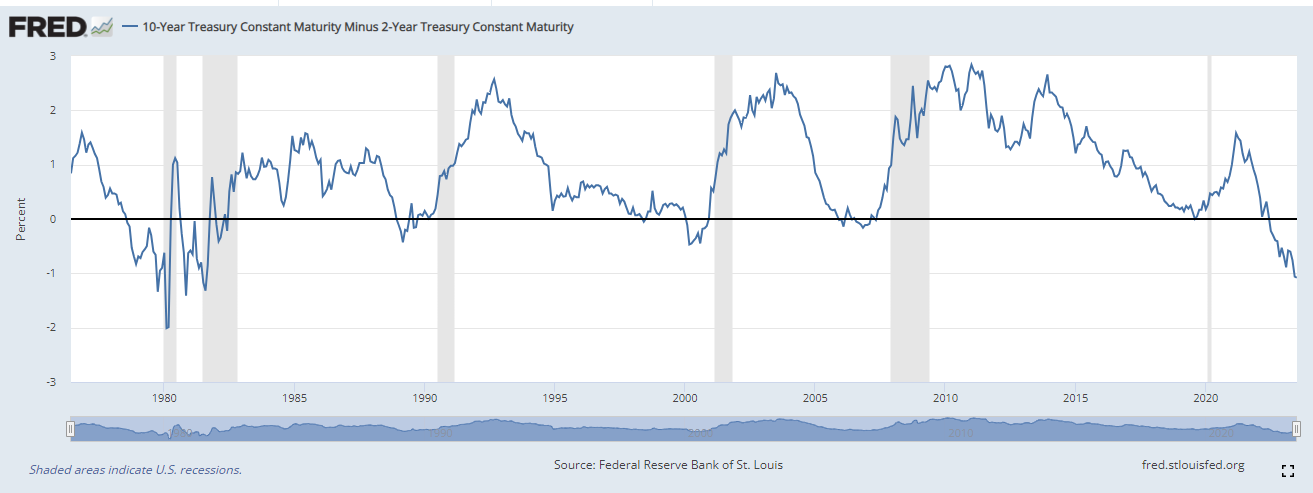

That pesky yield curve is still inverted

The spread between 2- and 10-year U.S. Treasury yields is deeply inverted, with its -1.08% spread the largest since 1981.

Historically, inversions are often followed by recessions. However, the FOMC’s most recent summary of economic projections does not appear to be forecasting a recession.

Still, this disconnect between economic history and economic forecast implies a degree of uncertainty that may not be priced in by markets.

As an investor with a bullish bias, it forces me to ask, “What if I’m wrong?” I don’t think I’m alone. As more investors ask this question, a reluctance could grow when it comes to deploying capital to crypto assets.

That, in and of itself, could serve as a short-term hurdle for crypto prices.

From CoinDesk Deputy Editor-in-Chief Nick Baker, here is some news worth reading:

-

BLOCK SCHOLES: It doesn’t take too long hanging around finance before you hear the words “Black-Scholes,” the famous options pricing model. I’ve even seen it argued that it’s one of the most important math formulas of the past century. Anyway, when you spot a headline with “Block Scholes,” you start wondering if that’s a typo of Black-Scholes. But, no, it’s a crypto data firm, and a recent CoinDesk story explains that it has determined that crypto prices have untethered from stocks. I’d argue this is either really good news for macro investors looking for uncorrelated assets or terrible news for crypto traders adrift in a sea of bad news.

-

POOR APES: Another formerly hot area, Bored Ape Yacht Club NFTs, are getting hit hard lately, with the floor price of the BAYC collection sinking to a 20-month low. This fits with the recent trend in crypto: while the heavyweights, bitcoin and ether, are doing great, much of the rest of the industry is struggling.

Edited by Nick Baker.