Bitcoin Mining And ERCOT – The Data Tells The Story

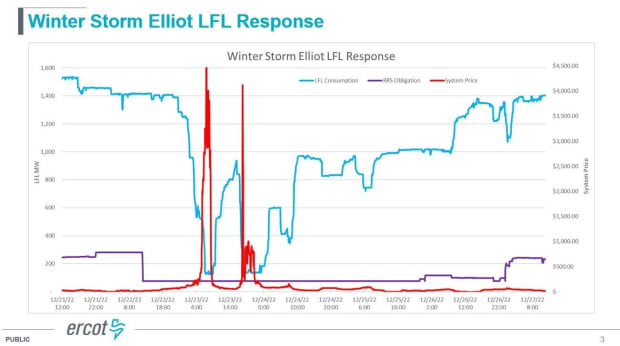

Several headlines recently described a 25% drop in bitcoin network difficulty during Winter Storm Finn in January. Most attributed this drop to curtailment activity in Texas. While Texas does represent 17% of the global bitcoin hashrate, ERCOT data shows that some of the curtailment activity was a combination of higher prices and “good grid citizenship.” In ERCOT, and to a lesser extent in other ISOs, prices are the best proxy for grid stress. There are other proxies such as PRC (physical responsive capability) but prices are a better measure for most situations. For that reason, in order to prevent swings in prices and create more challenging gird conditions, an optimal environment is one in which the price does not swing wildly up and down. However, price volatility is a frequent occurrence in ERCOT, as evidenced by Winter Storm Elliot in December 2022 (see graph below).

Bitcoin miners are the economically perfect consumers of electricity. That is not to say that bitcoin miners will consume electricity in an altruistic way, but rather that margins for bitcoin miners are uniquely sensitive to the price of power such that they are economically incentivized to curtail consumption when power prices exceed their breakeven threshold (current breakeven for most miners ranges between $100 and $200 per MWh). That means they will consume electricity when prices are below their breakeven price and turn off when prices are above it. There are some operational and practical exceptions to this, for example, if miners have data center colocation agreements that stipulate or guarantee uptime.

Texans should want bitcoin miners to be on anytime power is abundant because their consistent consumption incentivizes the buildout of additional generation. And less counterintuitively, we naturally want bitcoin miners to curtail when prices are high and the grid is under stress.

That brings us to the January 2024 winter event of the week of January 15th. The headlines would have you think that the Texas grid was again stressed and that bitcoin miners curtailed as a result. The truth is much more nuanced. The average settlement price in the ERCOT wholesale power market during the worst three days of the storm was $100.76 per MWh, and prices never exceeded $600 per MWh. For context prices max out at $5,000 per MWh. As indicated by wholesale prices, the grid weathered the storm quite well with ample reserves throughout.

ERCOT did indeed issue a conservation alert, but that was more of a precautionary message for power consumers who don’t monitor the power price every second of every day like bitcoin miners do.

We did see some economic curtailment, meaning curtailing power usage based on price signals, from miners for extended periods, and some shorter periods when the prices exceeded $200 MWh. However, this activity was less pronounced than in previous winter events or summer heat waves because generation reserves were more abundant across the grid. Some bitcoin miners likely curtailed for longer periods as a gesture of good “grid citizenship,” and to show their commitment to a stable grid, but that is hardly quantifiable.

All of this evidence indicates that the difficulty drop last week necessitates a more nuanced explanation. Much of it was a result of curtailment in Texas, but after evaluating ERCOT pricing data, it leads me to believe that a material portion of that curtailment came from other ISOs in North America as well. In short, everyone who has an opinion about bitcoin mining curtailment would do well to watch ERCOT settlement and LMP prices. The data and the economics should form the backbone of all future analyses.

This is a guest post by Lee Bratcher. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.