Bitcoin Is On FIRE

The ethos of living frugally and investing wisely only gets better when applied to a bitcoin standard.

What is FIRE?

Financial Independence, Retire Early (FIRE) is a movement focused on extreme savings and investment with the aim of allowing people to retire much earlier than conventional strategies target.

Extreme frugality is at the core of FIRE. Proponents aim to save significant amounts of their income — well over 50% in many cases. This is typically achieved through a disciplined focus on reducing expenses. Increasing income is encouraged, but acknowledged as less controllable than ruthlessly cutting spending.

Once their savings goal is achieved, retirees live off small periodic withdrawals. Most would apply the “4% rule” or something similar in order to calculate their savings goal and safe withdrawal amounts. Savings are typically invested almost entirely in equity index funds.

There is a huge amount of information available on FIRE that isn’t worth repeating here. You can do your own research, perhaps starting with one of the most popular FIRE bloggers – Mr. Money Moustache.

The Good: FIRE And Freedom

The FIRE movement has a lot going for it. Its biggest strengths stem from the low time preference behavior it encourages, much like bitcoin. FIRE proponents are willing to sacrifice immediate expenditure and make lifestyle compromises for the potential of increased future returns (by compounding savings) that will later enable a lifestyle of freedom. FIRE’s extreme frugality pairs well with minimalism and there is a degree of overlap between these movements. A common thread is the desire for freedom in its many forms — again something familiar to many bitcoiners. A minimalist lifestyle and mentality can provide a psychological sense of freedom well before retirement is achieved. Your possessions stop owning you and you can focus on the things you value most, even if you haven’t yet won complete control over your time.

The FIRE community is also ruthless at reducing management fees on their investments, almost always seeking out the lowest-cost options. They’ll be pleased to learn that bitcoin can be stored virtually for free in a fully self-sovereign manner in perpetuity. Even the lowest cost Vanguard or BlackRock equities ETF will be more expensive than holding the equivalent dollar value in bitcoin.

The Bad: It Might Not Work For Much Longer

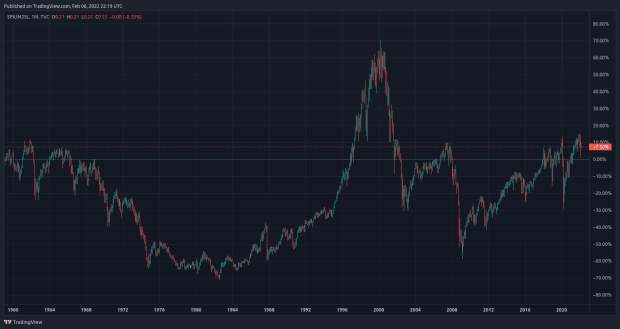

FIRE proponents typically invest almost all of their savings in equity index funds. This is potentially a problem if the money printer is turned off by central banks, as demonstrated by a chart of the S&P 500 denominated in USD M2 money supply which shows essentially flat performance over multiple decades:

FIRE proponents’ calculations could stop working if the fiat currency system fails and hyperbitcoinization arrives. As most bitcoiners know already, everything has been trending to zero when priced in bitcoin, including the S&P 500.

The Best Of Both Worlds: Bitcoin On FIRE

“I don’t think there is a single person with a negative opinion on bitcoin who has spent 100 hours studying it.” – Michael Saylor

Like all asset owners, the FIRE movement has been a beneficiary of the fiat standard. If it ain’t broke, don’t fix it …

But perhaps if FIRE proponents did their 100 hours they may find an incredible alignment between bitcoin and their personal values, as well as discovering investment fundamentals that are nearly bulletproof and make bitcoin the ideal savings vehicle.

Common critiques of bitcoin by the FIRE community are no different from those dished up by traditional finance circles over the past decade: bitcoin has no intrinsic value, it produces no cash flows, it is too volatile. Even if you accept these arguments as being deal-breakers to implementing a FIRE strategy (I don’t and I doubt most will after their 100 hours), they are all blown out of the water simply by bitcoin’s superior total returns.

It’s often said to be sacrosanct to sell bitcoin and I generally accept holding for as long as possible and supporting your lifestyle through productive work is likely to be the safest strategy for most people. However, retiring early and drawing down on your bitcoin holdings periodically into perpetuity will be mathematically possible for many, both sooner than they might imagine and before hyperbitcoinization. It simply requires bitcoin’s growth rate to exceed that of your withdrawals and inflation. As Greg Foss says: “It’s just math.”

I encourage you to run your own numbers (everybody’s situation is different and this is not financial advice). If you need help with a very basic spreadsheet template please reach out via Twitter.

Bitcoin’s historical total return performance has been incredible. Its 10-year compound annual growth rate (CAGR) is 200%. However, its increasing maturity could ultimately result in longer cycles with lower returns (fair to say the jury is still out on this!). Regardless, 200% provides a lot of wriggle room when you consider the S&P 500’s 10 year CAGR is ~13%. When running your numbers it would be prudent to build in your own buffers (for example, assume lower bitcoin returns in the future and/or higher rates of inflation into your expenses).

For those who are brave and trust in math, you’ll find you require a significantly lower starting balance when valued in fiat compared to using traditional FIRE techniques.

Bitcoin’s total return potential is also the best defense against volatility when retiring on a bitcoin standard in a fiat world. However, it may also be prudent to ensure withdrawals are regular (for example weekly or monthly) as you naturally wouldn’t want lumpier sales to coincide with periods of increased downside volatility in the bitcoin price. Psychologically this can be a difficult process to manage. A disciplined and consistent approach to sales – regardless of short-term price action – could help alleviate this tension. It’s essentially the opposite to buying bitcoin using dollar-cost-averaging (DCA) strategies (without the help of automated services).

For retired Bitcoiners from the Michael Saylor school who agree bitcoin will increase in value “… forever Laura” (my view too), delaying sales as much as possible will likely perform better over longer time frames. It just comes with more potential for anxiety and human error.

In conclusion, the typical FIRE template is not necessarily broken, but I contend there could be a better way for that movement. Simply replacing equity index funds with bitcoin (even in part) has the potential to significantly accelerate their path to freedom.

For existing Bitcoiners, running some basic numbers on retirement is always worth doing, even if you never intend to sell your bitcoin and would love to work forever. At the very least, afterwards you might feel like you aren’t short bitcoin … for a day or two!

This is a guest post by John Tuld. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.