Bitcoin, Ether Fall Outside Howey Test Criteria

Will the application of the “Howey Test” spark the next bullish move in cryptocurrencies?

There’s always something worth examining within the digital asset landscape. One day the topic du jour may be market structure, while the next day, it may be the underpinning technology and on other days…like Wednesday, securities law may engage you.

During my past life as an equity research analyst, 99.9% of what I considered daily, was “security.” With crypto assets, it hasn’t been that straightforward. And with the growing regulatory scrutiny targeting the sector, the definition of what is and is not a security has taken center stage.

In my opinion, a public, transparent definition and application of what constitutes a security is a net positive for crypto markets.

Clarity is paramount, and more of it will benefit all involved, most notably holders and potential holders of crypto assets.

What is the Howey Test? While straightforward on the surface, it can also present as a Rorschach test, its interpretation being left to the individual making the evaluation. Ultimately the Howey test determines what is and is not a security, using four prongs.

-

An investment of capital

-

In a common enterprise

-

With the expectation of profit

-

Driven by the efforts of others

If an asset meets all four prongs of the Howey Test, then it’s a security, and is thus required to register with the SEC, under requirements of the Securities Act of 1933 and 1934. If an asset does not meet those prongs, then it’s not. And from those four prongs, millions of dollars in legal fees will accrue.

The test has grown increasingly important lately, as the Securities and Exchange Commission (SEC) has placed the securities label on a number of cryptocurrencies.

Doing so puts those assets and any group facilitating their transfer under the SEC’s jurisdiction..

The SEC’s “Framework of Investment Contract Analysis of Digital Assets” whitepaper implies that digital assets satisfy the first two prongs. First, investors can purchase and/or acquire digital assets in exchange for something of value. Second, the SEC argues that in evaluating digital assets, a “common enterprise typically exists.”

Because cryptos meet these criteria, the SEC can now target them, particularly those connected to a central entity, and/or issued for the purpose of raising capital.

For example, the SEC likely considers Solana’s SOL a security partly because of the existence of the Solana Foundation, and its board of directors. The Solana Foundation has rejected the SEC’s characterization.

The third and fourth prongs are where things get interesting, particularly for bitcoin (BTC) and ether (ETH). In many ways, these criteria appear to differentiate bitcoin from ether and other tokens.

The SEC’s white paper on digital assets carves out “responsibilities performed and expected to be performed by an associated person (AP), rather than an unaffiliated, dispersed community of network users”.

The SEC also stated that AP’s of securities create or support a market for or the price of the digital asset, including its creation or issuance, or control of supply.

Bitcoin and ether maxis should find comfort within these areas.

While some market observers believe that the SEC’s latest regulatory push is targeting crypto as a whole, bitcoin and ether – the two largest cryptos in market value appear to fall outside this growing scrutiny, if applying the Howey test. And the SEC conspicuously omitted both assets from any lists potentially catergorizing them as securities. Indeed, the decentralized nature of governance and issuance makes them more akin to commodities than securities.

Bitcoin and ether currently account for close to 70% of all of the cryptocurrency market’s capitalization. Since the SEC’s announced suit against Binance, BTC’s market cap dominance has increased 3%.

ETH’s market share has fallen from 20.52% to 20.1% with bitcoin fueling the decline. In the aggregate their combined market cap dominance increased by approximately 2%, while their correlations between each other rose 6%.

While bitcoin has been labeled digital gold and ether digital oil, a better term for both may be digital water. The immutable nature of their code would represent its solid state, and its ability to adapt and adjust to multiple regulatory scenarios represents its liquid state.

In an odd way, the Howey Test seeming inapplicability is what may ultimately provide confidence for newer investors and leave the SEC focusing on a shrinking piece of the pie.

Time to Monitor Crypto Liquidity

In crypto markets, a lot of the attention is focused on scrutinizing price gyrations, sometimes overshadowing the significance of underlying liquidity trends. Adding such lenses can allow market participants to navigate the market better and understand where we stand in the cycle.

Price movements on thin volumes generally indicate a lower-quality signal than those accompanied by higher trading volumes. Thin volume signifies limited market participation at a specific price level, potentially leading to increased price volatility and reduced market depth. Conversely, higher trading volumes reflect broader market participation that indicates a more robust consensus and provides a more reliable foundation for price movements, thus enhancing the credibility of the signal.

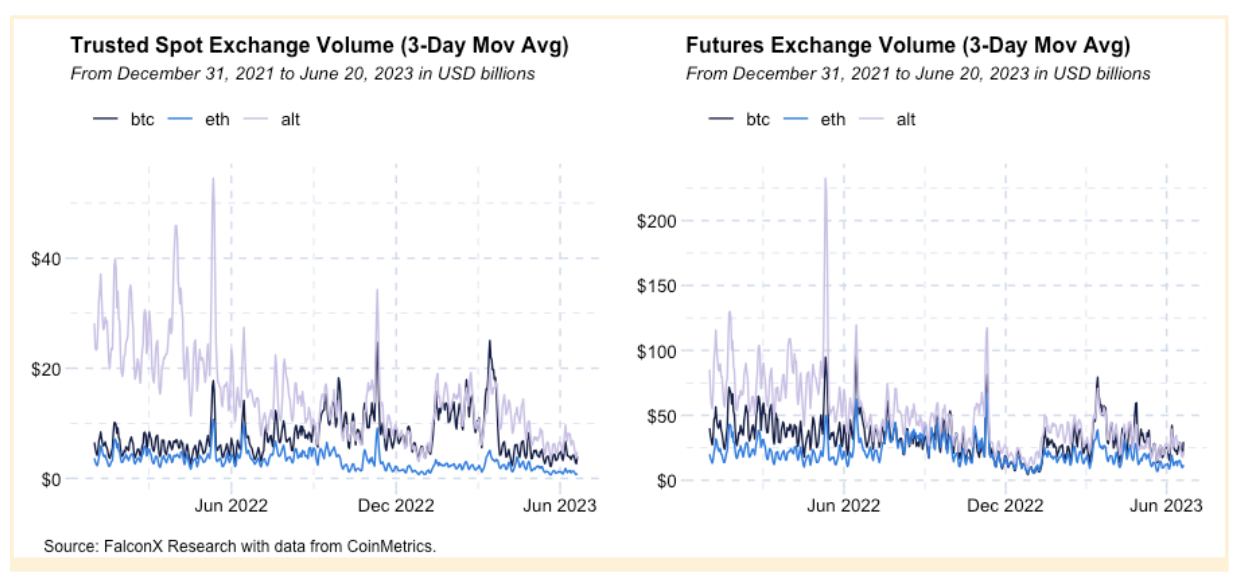

As shown below, crypto trading volumes have generally been trending south for spot (left) and futures (right).

Some cases are related to changes in market structure and not investor preferences, including the significant decrease in BTC volumes in March 2023 after Binance ended its zero-fee trading policy for some key market pairs.

Other cases reflect a shift in market preferences. With few exceptions, trading volumes of assets aside from BTC and ETH have dropped most sharply, as investors rotate to the more battle-tested investment cases. Among the more prominent names, the shrinking liquidity trend has been especially evident for DOGE, Litecoin (LTC) and SOL.

Interestingly, however, these liquidity trends are showing early signs of stabilization or even reversal in some cases.

Spot trading volumes, the segment hardest hit in 2023, have been practicing a slight recovery and now stand a tad above 2022 volume lows. Still, that’s an improvement from the recent volume prints that marked the lowest levels since late 2020.

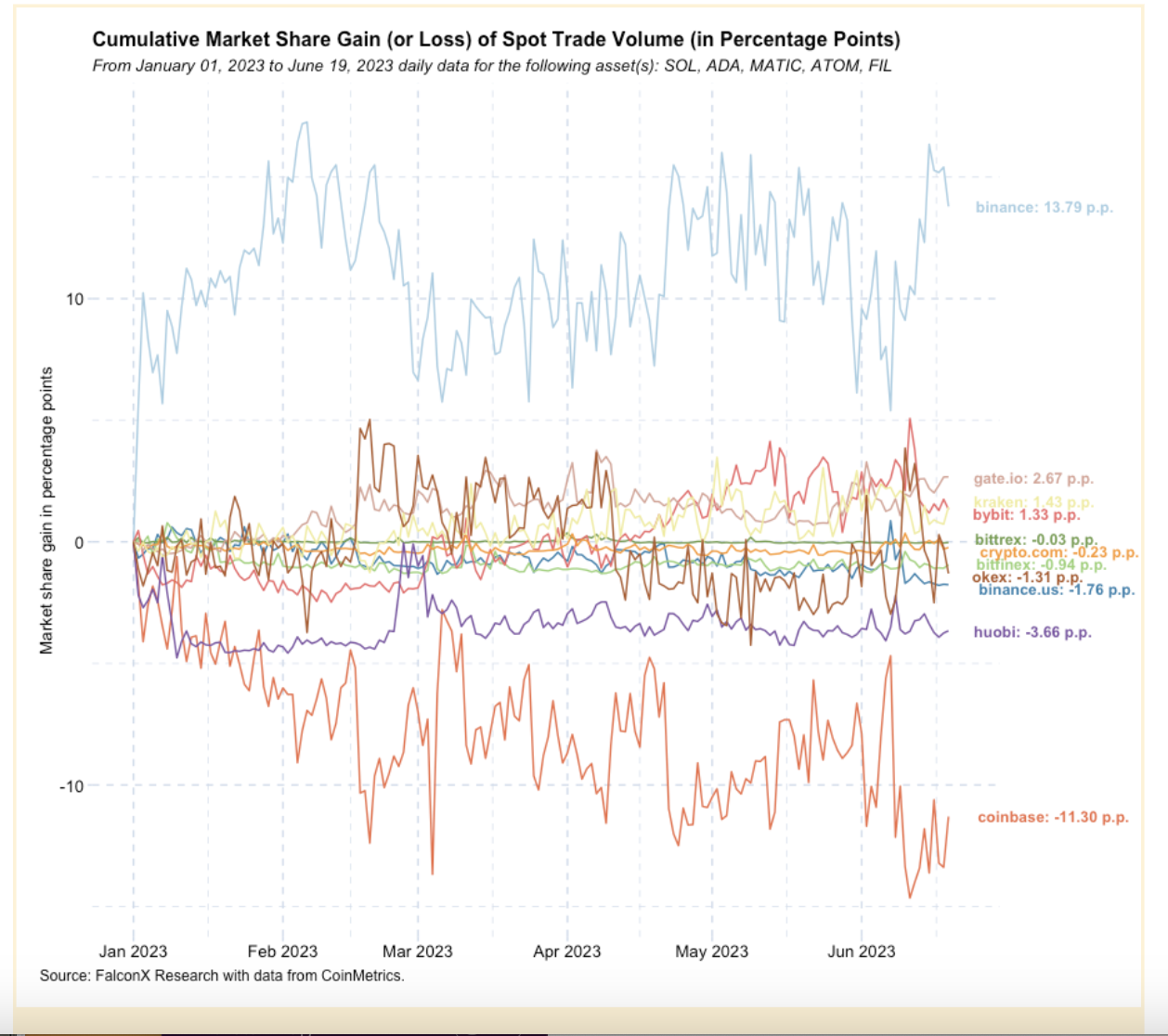

This slight recovery in spot volumes has been accompanied by market depth. Orderbook depth, another critical liquidity metric, has improved since the beginning of May for BTC and ETH (more so for the latter than the former). This recovery is noteworthy because it follows extensive reports of two top crypto liquidity providers curtailing their U.S. trading activity, which would, all else equal, imply a deterioration of order book depth instead of the improvement we have seen.Among non-BTC and non-ETH assets, the market’s focus on liquidity is related to the impact on some of the assets mentioned in the SEC charges against Coinbase and Binance. Two weeks since the news broke, trading volumes in the five most prominent assets by market capitalization (SOL, ADA, MATIC, FIL, and ATOM) have not changed significantly. The most notable shift in these assets has been how trading activity seems to have moved from the U.S. to international markets since the beginning of the year, as the chart below shows.

Bear markets tend to end not with a bang but with a whimper. Indifference and apathy are the typical defining signatures of the last stage of the bear market psychology framework –denial, anger, bargaining, depression, and acceptance –that we borrowed from psychologists.

Judging from the state of crypto market liquidity, we’re deep in the fifth stage of grief territory. But some of the early signals of potential stabilization, or even a timid reversal, are interesting. Sustained recoveries in crypto market liquidity have been early confirmation signals of bull markets in the past two cycles. We are not seeing such signals just yet, but the time to start keeping monitoring them could be now.

From CoinDesk Managing Editor Markets The Americas James Rubin, here’s some news worth reading:

-

THE SURGE: Bitcoin broke $30,000 for the second time this year amid bullish sentiment in the market following a number of traditional finance (TradFi) players pushing further into crypto.

-

BLACKROCK SEEKS A SPOT: The iShares unit of fund management giant BlackRock (BLK) filed paperwork Thursday afternoon with the U.S. Securities and Exchange Commission (SEC) for the formation of a spot bitcoin (BTC) ETF.

-

DEUTSCHE APPLICATION: Financial services giant Deutsche Bank AG has applied for regulatory permission to operate as a crypto custodian in Germany, the bank said Tuesday. The move came just days after asset management giant BlackRock filed with the SEC to create a spot bitcoin ETF. “I can confirm that we applied for the BaFin license for crypto custody,” a Deutsche Bank spokesperson told CoinDesk, referring to Germany’s financial regulator.

-

TOKENS AS SECURITIES?: CoinDesk columnist Daniel Kuhn asks “what could users do with a token that’s been labeled a ‘security?’” Kuhn writes that if a blockchain is “sufficiently decentralized,” then consumers should be able to trade the token and use its source code. “So what can a user do with a token that is a security?” Kuhn asks. “Everything you could with a token before it was declared a security.”

Edited by James Rubin.