The debate around whether or not this policy is a form of quantitative easing misses the point: Liquidity is the name of the game for global financial markets.

The article below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

QE Or Not QE?

The Bank Term Funding Program (BTFP) is a facility introduced by the Federal Reserve to provide banks a stable source of funding during times of economic stress. The BTFP allows banks to borrow money from the Fed at a predetermined interest rate with the goal of ensuring that banks can continue to lend money to households and businesses. In particular, the BTFP allows qualified lenders to pledge Treasury bonds and mortgage-backed securities to the Fed at par, which allows banks to avoid realizing current unrealized losses on their bond portfolios, despite the historic rise in interest rates over the past 18 months. Ultimately, this helps support economic growth and protects banks in the process.

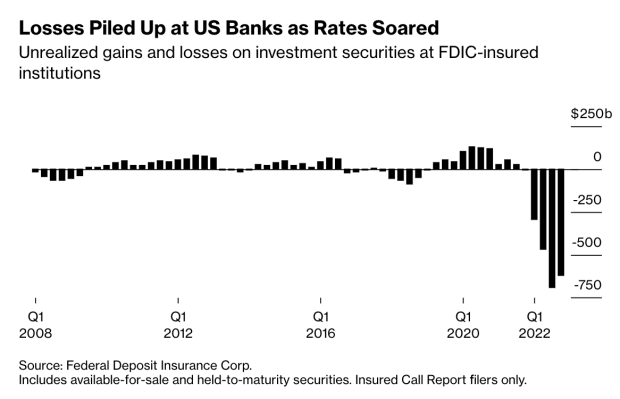

The cause for the tremendous amount of unrealized losses in the banking sector, particularly for regional banks, is due to the historic spike in deposits that came as a result of the COVID-induced stimulus, just as bond yields were at historic lows.

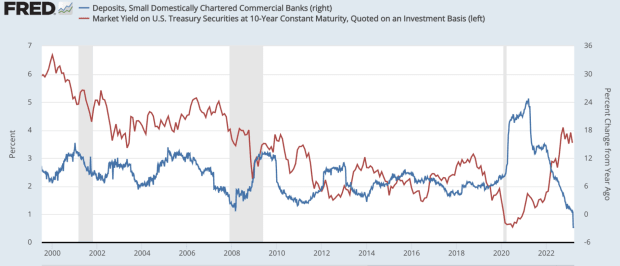

Shown below is the year-over-year change in small, domestically chartered commercial banks (blue), and the 10-year U.S. Treasury yield (red).

TLDR: Historic relative spike in deposits with short-term interest rates at 0% and long-duration interest rates near their generational lows.

Banks saw a spike in deposits with short-term interest rates at 0% and long-duration interest rates near their generational lows.The rise in Treasury yields led to massive unrealized losses for banks holding bonds.Source: Bloomberg

The reason that these unrealized losses on the bank’s security portfolios have not been widely discussed earlier is due to the opaque accounting practices in the industry that allow unrealized losses to be essentially hidden, unless the banks needed to raise cash.

The BTFP enables banks to continue to hold these assets to maturity (at least temporarily), and allow for these institutions to borrow from the Federal Reserve with the use of their currently underwater bonds as collateral.

The impacts of this facility — plus the recent spike of borrowing at the Fed’s discount window — has brought about a hotly debated topic in financial circles: Is the latest Fed intervention another form of quantitative easing?

In the most simple terms, quantitative easing (QE) is an asset swap, where the central bank purchases a security from the banking system and in return, the bank gets new bank reserves on their balance sheet. The intended effect is to inject new liquidity into the financial system while supporting asset prices by lowering yields. In short, QE is a monetary policy tool where a central bank purchases a fixed amount of bonds at any price.

Though the Fed has attempted to communicate that these new policies are not balance sheet expansion in the traditional sense, many market participants have come to question the validity of such a claim.

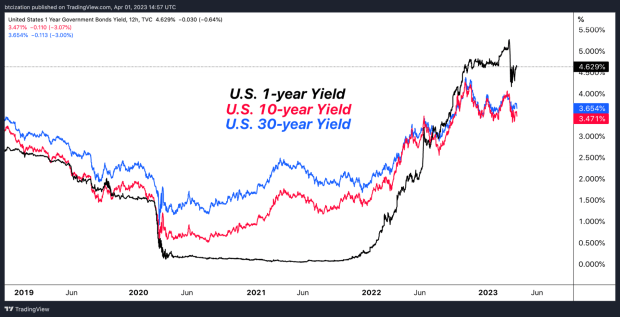

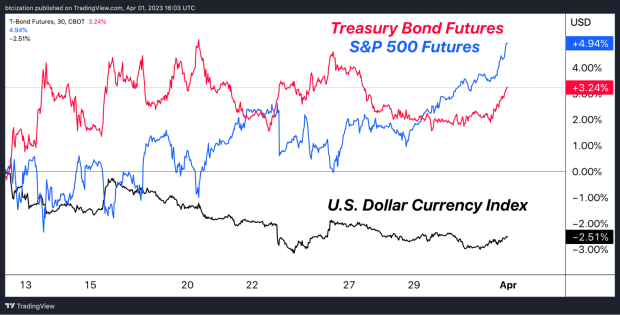

If we simply look at the response from various asset classes since the introduction of this liquidity provision and the new central bank credit facility, we get quite an interesting picture: Treasury bonds and equities have caught a bid, the dollar has weakened and bitcoin has soared.

Treasury bonds and equities caught a bid while the dollar weakened.Bitcoin soared with the liquidity being added into the system from the BTFP.

On the surface, the facility is purely to “provide liquidity” to financial institutions with constrained balance sheets (read: mark-to-market insolvency), but if we closely examine the effect of BTFP from first principles, it is clear that the facility provides liquidity to institutions experiencing balance sheet constraint, while simultaneously keeping these institutions from liquidating long-duration treasuries on the open market in a firesale.

Academics and economists can debate the nuances and intricacies of Fed policy action until they are blue in the face, but the reaction function from the market is more than clear: Balance sheet number go up = Buy risk assets.

Make no mistake about it, the entire game is now about liquidity in global financial markets. It did not used to be this way, but central bank largesse has created a monstrosity that knows nothing other than fiscal and monetary support during times of even the slightest distress. While the short-to-medium term looks uncertain, market participants and sidelined onlookers should be well aware as to how this all ends.

Perpetual monetary expansion is an absolute certainty. The elaborate dance played by politicians and central bankers in the meantime is an attempt to make it look as if they can keep the ship afloat, but in reality, the global fiat monetary system is like an irreversibly damaged ship that’s already struck an iceberg.

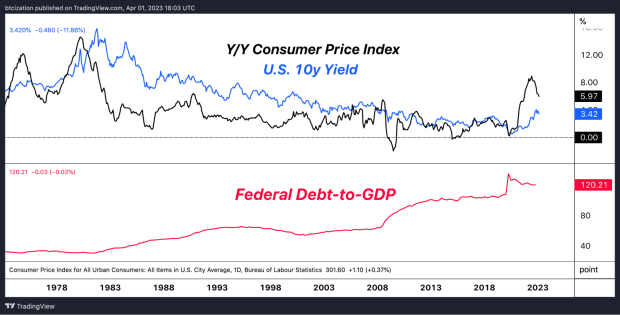

Let us not forget that there is no way out of 120% debt-to-GDP as a sovereign without either a massive unforeseen and unlikely productivity boom, or a sustained period of inflation above the level of interest rates — which would crash the economy. Given that the latter is extraordinarily unlikely to occur in real terms, financial repression, i.e., inflation above the level of interest rates, appears to be the path going forward.

CPI continues to run hot at the same time the debt-to-GDP ration is incredibly high.

Final Note

For the layman, there is no dire need to get caught up in the schematics of the debate whether recent Fed policy is quantitative easing or not. Instead, the question that deserves to be asked is what would have happened to the financial system if the Federal Reserve didn’t conjure up $360 billion worth of liquidity from thin air over the last month? Widespread bank runs? Collapsing financial institutions? Soaring bond yields that send global markets spiraling downwards? All were possible and even likely and this highlights the increasing fragility of the system.

Bitcoin offers an engineering solution to peacefully opt out of the politically corrupted construct colloquially known as fiat money. Volatility will persist, exchange rate fluctuations should be expected, but the end game is as clear as ever.

That concludes the excerpt from a recent edition of Bitcoin Magazine PRO. Subscribe now to receive PRO articles directly in your inbox.

Relevant Past Articles:

Another Fed Intervention: Lender Of Last Resort

Banking Crisis Survival Guide

PRO Market Keys Of The Week: Market Says Tightening Is Over

Largest Bank Failure Since 2008 Sparks Market-Wide Fear

A Tale of Tail Risks: The Fiat Prisoner’s Dilemma

The Everything Bubble: Markets At A Crossroads

Not Your Average Recession: Unwinding The Largest Financial Bubble In History

The election is over, and Trump is now going to be President again. He pulled off something that hasn’t been done since Grover Cleveland in the 1800s, a successful re-election following a loss after his first term. People all of this space are celebrating this as some kind of victory for Bitcoin, but nothing could

The first bitcoin exchange-traded products (ETPs) have debuted trading on the London Stock Exchange after receiving approval from the UK's Financial Conduct Authority. Asset managers WisdomTree and 21Shares both listed bitcoin ETPs on the LSE today.NEW: 🇬🇧#Bitcoin ETPs will start trading on the London Stock Exchange today.Are you prepared? 👀 pic.twitter.com/llurxr1NjC— Bitcoin Magazine (@BitcoinMagazine) May

An announcement was put out today by the Justice Department that Keonne Rodriguez and William Hill had been arrested and charged with operating Samourai Wallet, “an unlicensed money transmitting business” that executed “unlawful transactions.”Fuck the Justice department, full stop. At no point did Samourai custody user funds, have control over user funds, and ESPECIALLY did

In a recent SEC filing, Tesla explained bitcoin’s liquidity use case while outlining its “long-term potential.”In a recent SEC filing, Tesla doubled-down on its bitcoin investment as “a liquid alternative to cash” thesis.Tesla experienced a rocky path from buying bitcoin, to accepting it as payment, and later removing it as a payment method over environmental…

What are some options for businesses looking to take advantage of the benefits Bitcoin has to offer?We’ve discussed a few points previously about adding Bitcoin to the treasury of a small business, in order to address inflation as well as provide other benefits. Of course, one could acquire Bitcoin by simply taking the U.S. dollar…

This article is featured in Bitcoin Magazine's "The Privacy Issue". Subscribe to receive your copy. With the Fourth Halving in the rearview mirror, it seems a perfect time to provide some on-record analysis of Bitcoin from the perspective of Number and Time, aka Crypto-K, which is the name for a methodology my friend and I

Russell Okung is no bitcoin tenderfoot. The Los Angeles Chargers left tackle hosted his own Bitcoin event in September 2019 after he made a public splash onto the scene with his “Pay me in Bitcoin” tweet during the off-season. Now, for his December 8, 2019, matchup against the Jaguars, bitcoin will be with him every…

This article is featured in Bitcoin Magazine’s “The Inscription Issue”. Click here to get your Annual Bitcoin Magazine Subscription.A new inscriptionA Bitcoin script shoneA light on how it could be doneSo on our nodes it was runIs it on the way out?What are they about?It’s not an OP RETURNPerhaps we can learn.So it’s a message

Binance's bitcoin balance sees its largest one-day outflow ever and the price legitimacy for the exchange-native BNB token is called into question. The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine's premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis…