The nightmare of every NFT collector is losing their seed phrase. It’s hard to see a hacker steal your non-fungible tokens (NFTs), but it’s harder to see them sitting in a dead wallet, because you’ve got no one to blame but yourself.

Even worse, stolen NFTs can be recovered, but a dead wallet is forever. The NFTs are still yours, but you can’t sell them, because you can’t transfer them to a buyer’s wallet.

Brian Frye is a professor at the College of Law at the University of Kentucky, NFT artist and filmmaker.

So, how much is an NFT in a dead wallet worth? Everything and nothing. The NFT itself hasn’t changed, so presumably its value hasn’t changed either. After all, it still represents ownership of the same artwork. And yet, an NFT you can’t sell is functionally worthless. At least you can still enjoy the art?

While a dead wallet is a heartbreak for a collector, it could also be a headache for the collector’s heirs. There’s no sure way to abandon ownership of a dead wallet, so you own it until you die and it becomes part of your estate. And if your estate is large enough, it might be taxed on the value of the NFTs in the wallet, even though they can’t be sold. At least your heirs can break the chain by disclaiming the wallet.

Of course, this is a quintessential rich people problem. The federal estate tax exemption is currently $12.06 million for individuals and $24.12 million for married couples, so most of us have nothing to worry about. But sooner or later, a crypto billionaire is bound to leave a dead wallet stuffed with blue chip NFTs, and the taxman will come knocking.

What’s to be done? Is there any solution to this entirely theoretical but hopefully amusing problem? Maybe. But in order for it to make sense, you have to understand how property law perceives NFTs.

The asset doesn’t actually have any real market value, even though it theoretically should

One is the loneliest number

Legal scholars often describe property as “a bundle of sticks,” a metaphorical way of observing that property consists of a collection of discrete rights to use something. Each right is a stick in the bundle, and property owners can use those rights however they like. Among other things, property owners can remove sticks from the bundle of rights and license or transfer them.

But when it comes to NFTs, there’s usually only one stick: The right to transfer ownership. An NFT is essentially a cryptographic ledger entry that represents something other than a quantity of cryptocurrency. Ledger entries can represent literally anything, and NFTs are no exception. But most NFTs represent nominal “ownership” of a work of digital art.

What does that mean? Typically, artists create NFTs and simply declare that they represent ownership of artwork. And NFTs are valuable because the NFT market believes them. But most NFTs don’t give their owners any rights in the artwork they represent. The only thing NFT owners necessarily own is the right to transfer their NFT to someone else.

Apparently, that’s enough to make NFTs valuable. It shouldn’t come as a surprise. The only right art collectors have ever cared about is the right to transfer artwork. Everything else is surplusage. The only difference is that collectors transfer NFTs on the blockchain, rather than in person. Plus ça change.

And yet, sometimes the difference matters. It’s all well and good to transfer an NFT on the blockchain, until you can’t, because it’s in a dead wallet. From a legal perspective, you still own the NFT, because you still own the wallet, even though you can’t access it. But from the perspective of the NFT market, you don’t, because the only thing NFT collectors care about is whether you can transfer your NFT to their wallet.

Of course, property law says you can still transfer ownership of your NFT, simply by stating your intention to do so, irrespective of what the blockchain says. Unfortunately, the NFT market doesn’t value that kind of transfer, so the law doesn’t matter. Or at least, the law won’t help you find a buyer. But it might help in other ways.

Talking with the taxman about art

What about taxation? As Benjamin Franklin famously observed, “in this world, nothing is certain except death and taxes.” But even their certainty is greatly exaggerated. After all, no one knows when their hour will come, and no one knows what the IRS will bill. At least the IRS provides a facsimile of due process.

In any case, the taxation of NFTs is usually reasonably predictable. The IRS taxes art as “collectibles,” subject to a capital gain tax of 28%, and it taxes NFTs just like any other kind of art. So, if you sell an NFT for a profit, you have to pay a 28% tax on the capital gain. Expensive, but simple.

Owners of dead wallets are in luck when it comes to taxation. Sure, they can’t sell their NFTs for a profit, which is a major bummer. But if you can’t make a profit, there’s nothing to tax. Take that, Uncle Sam. But what happens when owners of dead wallets die? And what happens when a wallet dies with its owner?

Posthumous tokens

Imagine a wealthy NFT collector dies, leaving a wallet full of valuable NFTs. Under the law of succession, the wallet becomes part of the collector’s estate and passes to the collector’s heirs. But what if it’s a dead wallet? The IRS doesn’t care. The NFTs are still part of the estate and are still subject to estate tax, even though they can’t be sold. It sounds absurd, but we know it’s true, because it’s happened.

Robert Rauschenberg, “Canyon” (1959)

In 1959, Robert Rauschenberg created a “combine” or sculptural painting he titled “Canyon.” Among many other things, “Canyon” incorporated a stuffed golden eagle that Sari Dienes found in the trash and gave to Rauschenberg. Later that year, Rauschenberg showed the painting at the Leo Castelli Gallery, and art dealer Ileana Sonnabend bought it.

It was a coup for Sonnabend, because “Canyon” is widely considered one of Rauschenberg’s most important works. She exhibited it throughout the United States and Europe, including at the 1964 Venice Biennale, where Rauschenberg won the grand prize for a foreign artist. But her coup eventually became a catastrophe.

Enter the United States Fish and Wildlife Service, which became aware of “Canyon” in 1981, when Sonnabend shipped it back to the United States. The Bald and Golden Eagle Protection Act of 1940 prohibits the possession or sale of eagle carcasses, with very limited exceptions. In a nutshell, “Canyon” is illegal.

With Raushenberg’s help, Sonnabend got a special permit that allowed her to keep the eagle carcass. She still couldn’t sell “Canyon,” so instead she loaned it to museums, including the Baltimore Museum of Art and the Metropolitan Museum of Art in Manhattan. Problem solved, at least temporarily.

But when Sonnabend died in 2007, the bird came back. She left an estate worth more than $1 billion to her children Nina Sundell and Antonio Homem, which consisted primarily of artworks, including “Canyon.” The estate sold about $600 million worth of art in order to pay estate taxes, but it couldn’t sell “Canyon,” because of the eagle. So it valued the work at $0, because an artwork you can’t sell is worthless.

Owners of dead wallets are in luck when it comes to taxation…[I]f you can’t make a profit, there’s nothing to tax.

The IRS disagreed. It appraised “Canyon” at $65 million and assessed $29.2 million in estate tax. Unsurprisingly, the Sonnabend heirs objected, and the IRS eventually agreed to forgive the bill if the estate donated “Canyon” to a charity. So the heirs gave it to the Museum of Modern Art, and the problem was solved for good.

The Sonnabend saga is instructive primarily because it’s so absurd. The outcome was preordained, the heirs just didn’t want to accept it, and the IRS was too sclerotic to explain its expectations.

I assume (or at least hope!) the IRS will treat dead wallets the same way. An estate can’t sell the NFTs in a dead wallet. But there’s no reason it can’t transfer ownership of the wallet to a charity and avoid taxation.

Last year, my CoinDesk Tax Week op-ed focused on donating NFTs to art museums. Among other things, I observed that eligible NFT donors can take a charitable contribution deduction, and reflected on how to value donated NFTs for tax purposes. And in another CoinDesk op-ed, I argued that NFT collectors can donate dead wallets for a deduction. After all, they still own the wallet, even though they can’t use it.

Candidly, I’m a little skeptical the IRS will allow NFT collectors to take a charitable contribution deduction for donating a dead wallet. It’s too clever by half, because the asset doesn’t actually have any real market value, even though it theoretically should. But if the IRS values dead wallets at $0 for the purpose of the charitable contribution deduction, it ought to value them at $0 for the purpose of the estate tax as well. Here’s hoping.

As decentralized finance, or DeFi, continues to evolve and mature, the concept of total value locked – a measure of how much money users have stashed in a given protocol – has also gained significant attention. Originally focused on digital assets such as cryptocurrencies, TVL has expanded to include tokenized real-world assets (RWA), providing a

news Thailand’s anti-money laundering regulator is planning to amend the country’s laws to include cryptocurrency. Speaking to the Bangkok Post, Police Major General Preecha Charoensahayanon, secretary-general of the Anti-Money Laundering Office (Amlo), said he believes that, while currently not an issue, cryptocurrency “will be a tool of new money laundering.” Preecha said that Amlo currently does not receive complaints…

Good morning. Here’s what’s happening:Prices: Bitcoin retreats below $26.5K amid wider crypto decline as Binance, Coinbase-related fears linger.Insights: The decline in bitcoin and ether prices since 2022 mirrors the decrease in stablecoin balances over the same period.Bitcoin returned to its downtrodden ways on Wednesday amid a wider crypto decline that swept up altcoins mentioned and…

May 1, 2020 at 22:54 UTCUpdated May 1, 2020 at 22:55 UTCMISSING MONEY: iFinex, the parent company to Bitfinex and Tether, has filed for subpoenas to depose three banks across the U.S. that it believes held funds for Crypto Capital, Bitfinex's payment processor. (Credit: Shutterstock)Bitfinex, Tether Seek Subpoenas Across US in Hunt for Missing $800MThe…

The NYSE has withdrawn a proposed rule change to trade options based on bitcoin ETFs. Other exchanges have also withdrawn similar applications, but have also refiled. The operator of the New York Stock Exchange has withdrawn its application to list and trade options based on the Bitwise Bitcoin ETF and the Grayscale Bitcoin Trust, according

Additional charges levied against Sam Bankman-Fried in the U.S. face an extra delay, after a Tuesday Bahamas Supreme Court judgment allowed the FTX founder to judicially review the terms of his extradition from the Caribbean.Bankman-Fried has been under the legal spotlight after the collapse of his crypto exchange in November. After originally seeking his extradition…

news Enterprise blockchain startup Digital Asset (DA) has named co-founder Yuval Rooz as the company’s new chief executive officer. Rooz, who has served as both COO and CFO at the firm, takes over from acting CEO AG Gangadhar, who stepped in when its iconic leader Blythe Masters left last December. Digital Asset’s board of directors…

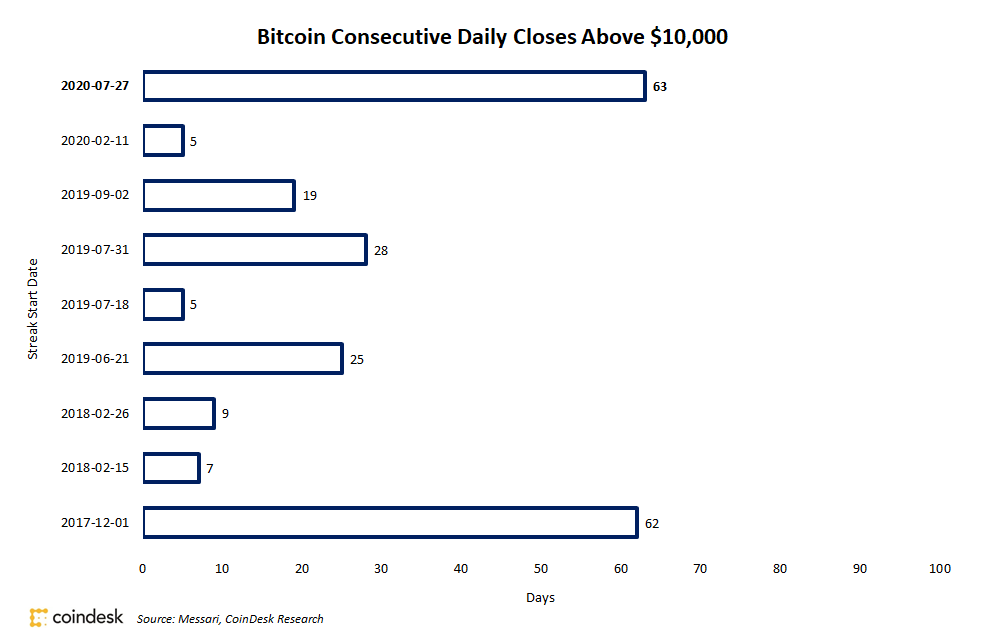

Sep 28, 2020 at 00:01 UTCUpdated Sep 28, 2020 at 00:13 UTCBitcoin streaks of days trading above $10,000Bitcoin closed Sunday at $10,793 setting a record of 63 consecutive daily closes above $10,000, according to market data aggregated by Messari.The bellwether cryptocurrency’s previous record 62-day streak above $10,000 lasted from Dec. 1, 2017, through Jan. 31,…

Aug 20, 2020 at 16:44 UTCUpdated Aug 20, 2020 at 17:23 UTCU.S. Rep. Tom Emmer (Al Mueller/Shutterstock)Rep. Tom Emmer of Minnesota will accept crypto donations for his campaign. The chairman of the National Republican Congressional Committee (NRCC) and member of the Congressional Blockchain Caucus opened his first cryptocurrency town hall on Thursday with the announcement,…

:format(jpg)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/M242SVBJV5DJJGZVNMFOJWSJMU.jpeg)